| home > report on operations > financial position > review of balance sheet, income statement and financial position |

home > report on operations > financial position > review of balance sheet, income statement and financial position

review of balance sheet, income statement and financial position

Income Statement

The Income Statement of the Parent

Company for financial year 2012

recorded a net loss of 245.7 million

euros, against a net profit of 39.3

million euros for financial year 2011,

mainly determined by the strong and

unexpected reduction of advertising

revenues (-209.0 million euros) and the

costs of big sports events.

As reported in greater detail further

ahead in this report, the 2012 result

benefits from a positive component

equating to 20.5 million euros deriving

from the adoption, as of this year, of the

valuation of investments at equity,

instead of evaluation at cost adopted

until 31 December 2011.

The reasons for this change arise from

the need to offer a better representation

of the financial and earnings situation

along with the results of operations and

to increase the consistency of the

Company’s equity, aligning equity

figures with those of the consolidated

financial statements.

This change also determines the

booking of a Shareholders’ equity

reserve of 112.1 million euros, by effect

of the change in principle adopted until

31 December 2011.

The following section provides an

overview of the main items of the

Income Statement and the reasons

behind the more significant changes

from the previous year.

Revenues from sales and services

Revenues from sales and services consist

of licence fees, advertising revenues and

other commercial revenues.

They totalled 2,625.5 million euros,

down 199.3 million euros (-7.1%) on

2011.

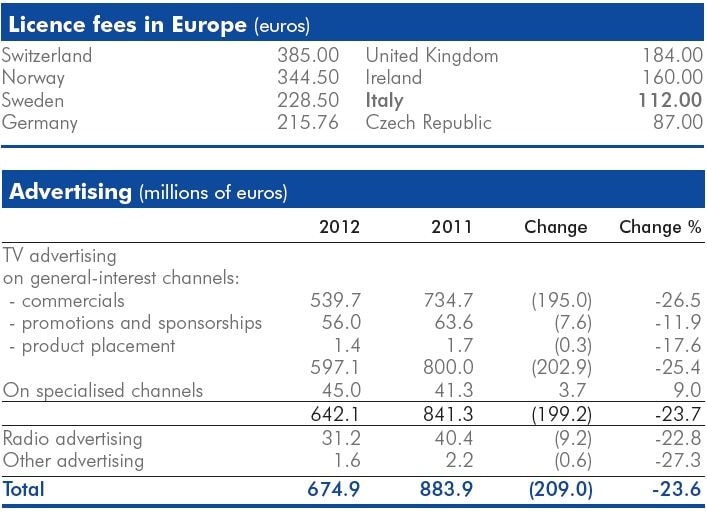

Licence fees (1,747.8 million euros).

These include licence fees for the

current year as well as those for

previous years, collected through coercive payment following legal

registration.

The overall increase (+2.3%) refers to the

increase in the per-unit licence fee from

110.50 euros to 112.00 euros (+1.4%)

and to the increase in the number of

paying subscribers due to the significant

growth in new subscribers compared to

the number of new subscribers in 2011

(506,486 units, +26.0%) capable of

offsetting the rise in cancellations and

arrears, or of the number of subscribers

entered in the list of debtors who have not

paid their licence fee.

Once again in 2012 the licence fee

paid in Italy continues to be one of the

lowest in Europe.

By way of example, the table shows the

annual licence fee, in euros, in force in

selected European countries.

Advertising revenues.

In a framework

characterised by the deceleration of the

economy and the drop in consumption,

advertising revenues in 2012 also

recorded evident signs of difficulty.

The Nielsen figures, while failing to

allow a fully standardised comparison

due to the fact that changes have been

made in the setting in which data is

measured, show a 14.3% contraction in

the advertising, affecting all media,

apart from the Internet, which closed at

+5.3%. Television and radio advertising

investments in particular show a decline

of 15.3% and 10.2% respectively.

In this context, Rai’s advertising

revenues (674.9 million euros) highlight

a reduction of 209.0 million euros

(-23.6%) compared with 2011, as

shown in the table to the right.

The drop in advertising revenues was

higher than the contraction of the

reference market, determining a

considerable loss of the market share by

the Rai concession holder during the

year. To offset this, incisive actions were

taken to intervene on the various

corporate areas of Sipra, including a

review of commercial practices and a

strengthening of the managerial layout

and of in-house procedures.

It should be noted that revenues from

advertising on specialised channels

continue to grow (+3.7 million euros,

+9.0%).

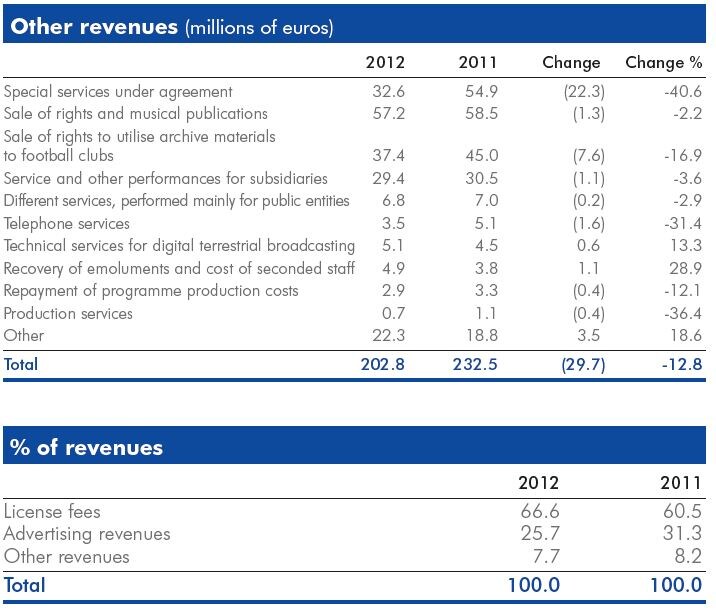

Other revenues present a reduction of

29.7 million euros (-12.8%), as

highlighted in detail in the table to the

right.

The reduction is determined mainly by

the drop in the Special services under

agreement item (-22.3 million euros),

resulting largely from reduction of

amounts provided by the Presidency of

the Council of Ministers to 50%

compared to that envisaged for the

previous year and by the Sale of rights

to utilise materials to football clubs item

(-7.6 million euros), the reduction of

which is due to different agreements

entered into during the two years.

Due to the advertising crisis and

because of the reduction of other

revenues, as indicated in the table to

the right, revenues from licence fees

represent two thirds of overall income.

Operating costs

The item includes internal costs (labour

cost) and external costs, regarding

ordinary business activities.

These total 2,535.2 million euros, up

18.1 million euros, (+0.7%), compared

with 2011, the reasons for which are

listed below.

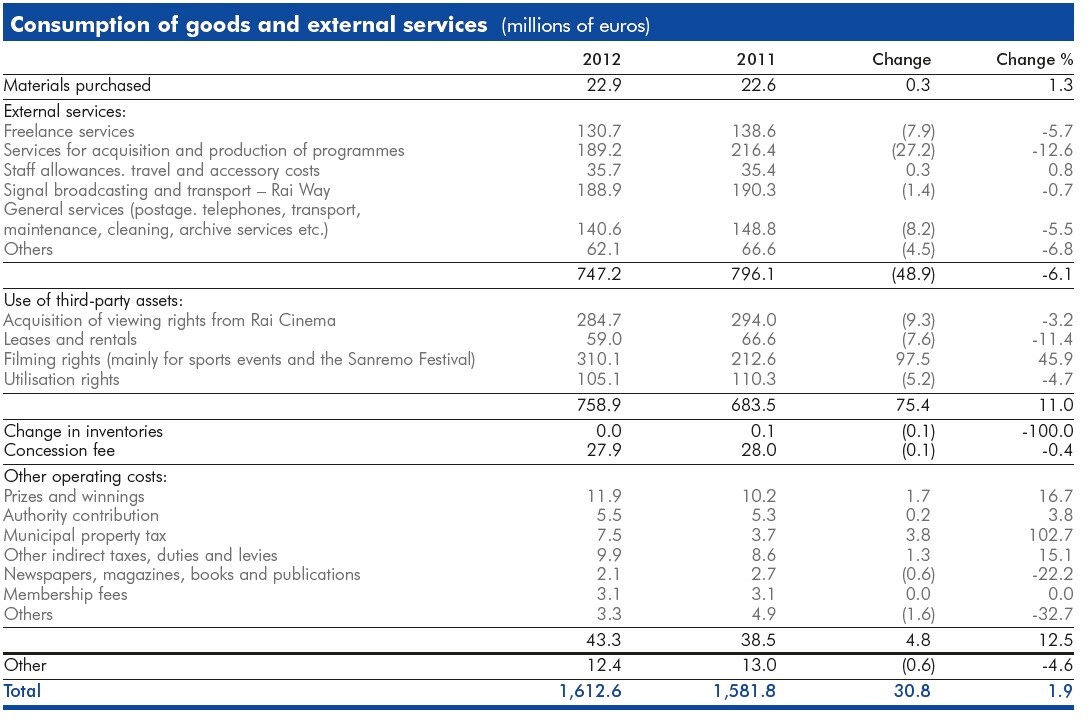

Consumption of goods and external

services – This caption includes

purchases of goods and services

required to make programmes of

immediate use (purchases of

consumables, external services, artistic

collaborations, etc.), filming rights for

sports events, copyright, services from

subsidiaries, running costs (rental and hire fees, telephone and postage costs,

cleaning, maintenance, etc.) and other

operating costs (direct and indirect

taxes, contribution to the Authority, the

public broadcasting concession fee,

etc.).

Compared with the previous year, the

item shows an increase of 30.8 million

euros (+1.9%), due to the presence

during the year of costs related to fouryearly

sports events (European Football

Championship and Olympic Games) for

143.0 million euros (including costs for

the production of these events

amounting to 8.1 million euros).

Net of this component, there was a net

reduction of about 110 million euros in

external costs compared to 2011, determined largely by initiatives

implemented during the year to contain

spending.

The table on the following page shows

details of savings in most items, apart

from filming rights which presents an

increase of 97.5 million euros for the

reasons already disclosed.

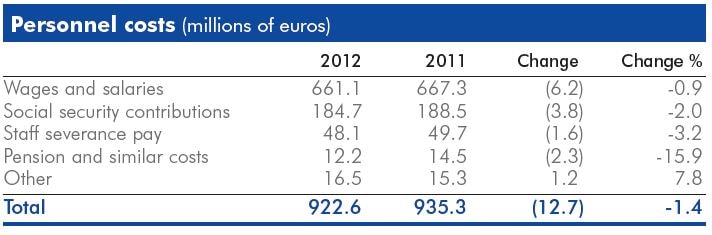

Personnel costs – These amount to

922.6 million euros, down 12.7 million

euros on the total at 31 December

2011 (-1.1%), according to the

breakdown in the table to the right.

The reduction in personnel costs is

determined mainly by the provision of a

bonus system for employees, about 19

million euros lower than that assigned in

the previous year.

Net of the phenomenon mentioned

above, personnel costs presented a

modest increase (about 6 million euros)

due to the positive effects of incentives

in 2011 which offset the physiological

growth in personnel costs as a result of

contractual automatic pay increases and

the impact of the renewal of the

collective labour contracts.

Lower inflation also positively influenced

the trend of personnel costs, having a

positive impact on the revaluation of the

provision for staff severance pay and the

continuation, once again in 2012, of

the substantial blockage of payment

policies.

Personnel on payroll at 31 December

2012 amounted to 10,476 units, up

280 on 31 December 2011.

The average number of employees,

including those on fixed-term contracts,

came to 11,851, with an increase of 22

members of staff compared to last year.

In details, there has been a drop of 214

members of staff on fixed-term contracts

following the final hiring of staff on

temporary contracts and an increase of

236 members of staff on permanent

contracts.

Gross Operating Margin

The Gross Operating Margin, as a

consequence of the above, is positive by

106.9 million euros, down 214.9

million euros, or -66.8%, on the

previous year.

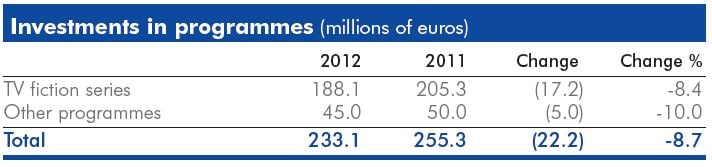

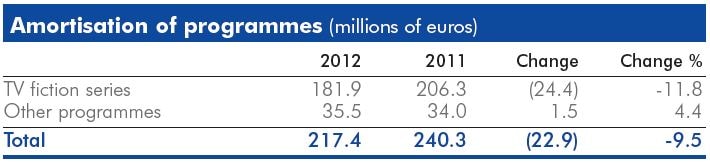

Amortisation of programmes

This caption is related to investments

in programmes, which during 2012

amounted to 233.1 million euros, down

22.2 million euros (-8.7%), largely for

TV fiction series.

Amortisationcharged to the above

captions for the year, 217.4 million

euros, shows a reduction of 22.9

million euros compared with the

previous year (-9.5%) related to the

trend in investments.

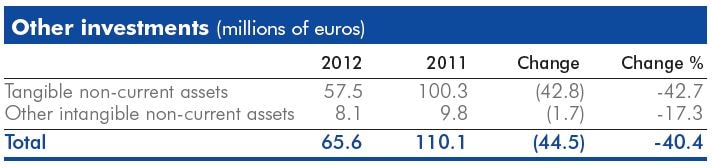

Other amortisation

The 2012 movement in this item, shown

in the following table, is linked to

investments in tangible non-current

assets and other investments, and

presents a total reduction of 44.5

million euros, largely determined by the

previous year’s acquisition of the DEAR

property complex for an amount of 52.5

million euros.

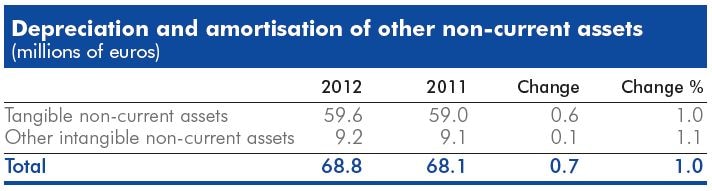

Amortisation and depreciation for the

period referring to the items mentioned

above amount to 68.8 million euros,

with a slight increase of 0.7 million

euros compared to 2011.

This substantial stability is due to the

offsetting effect between new

amortisation/depreciation due to

investments made during the year and

the reduction determined by the gradual

completion of the

amortisation/depreciation of assets

brought into use in past years.

Other net income (charges)

The item comprises costs/revenues not

directly related to the Company’s core

business and, in 2012, highlights net

expenses of 36.4 million euros (36.9

million euros in the previous year). In

detail, it comprises expenses for repeatusage

programmes which it is not

expected will be used, repeated or

commercially exploited (28.2 million

euros in 2011: 29.2 million euros),

provision for the company

supplementary pension fund for former

employees (12.0 million euros, in 2011:

13.8 million euros), provisions for risks

and charges (21.0 million euros, in

2011: 10.8 million euros), partially

offset by net contingent assets (20.5

million euros, in 2011: 18.1 million

euros) and the release of funds

allocated in previous years (10.3 million

euros, in 2011: 8.8 million

Operating Result

The performance described above for

operating revenues and costs led to a

reduction in the operating result, from

-23.5 million euros in the previous year

to -215.7 million euros this year, with a

deterioration of 192.2 million euros.

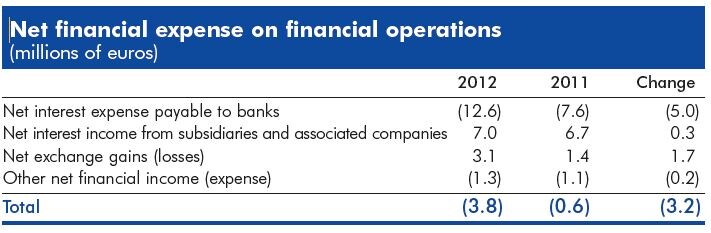

Net financial expense

Net financial expense shows a loss of

3.8 million euros (0.6 million euros in

2011). The item shows the economic

effects of typical financial operations

and comprises bank interest expense

and income as well as that relating to

Group companies and net gains in

relation to exchange rates.

The figures show an increase in net

interest payable to banks of 5.0 million

euros due to higher financial exposure

to third parties and an increase in the

average interest rates on loans.

Net intercompany positions, particularly

with Rai Cinema and Rai Way,

determined higher intercompany interest

income of about 7 million euros,

similarly to the previous year.

Exchange rate differences, mainly

generated by the acquisition of rights to

sports events in US dollars, were positive

and increased thanks partly to hedging

activities carried out in previous years,

which counteracted the fluctuations in

the euro/dollar exchange rate during

the year. Other financial expenses,

which grew modestly, deteriorated as a

result of higher bank commissions for

new loans.

The average cost of loans, consisting of

current account credit lines, ‘hot

money’, stand-by and medium-term

loans, settled at 3.4% (2.8% in the

previous year), up in relation to the

increased weight of fixed rate debts

compared to the previous year.

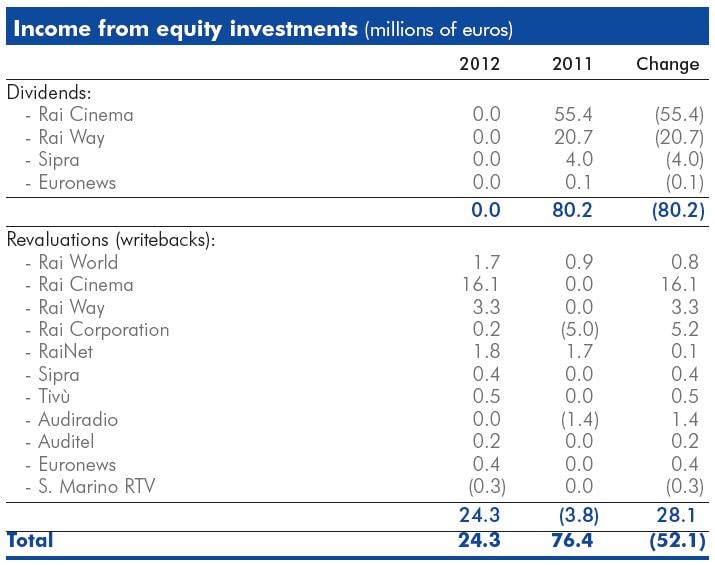

Income from equity investments

As indicated in the table on the

following page, the item amounts to a

total of 24.3 million euros.

As already highlighted, as of 2012

investments in subsidiaries and

associated companies are assessed

using the equity method instead of the

previous valuation method based on the

purchase cost adjusted in the event of

durable losses in value.

The equity method envisages that the

value at which investment is booked be

the same as the corresponding fraction

of the Shareholders’ equity resulting

from the last financial statements, minus

the dividends and after the adjustments

required by the principles used in the

preparation of the consolidated

financial statements.

The gain or loss by the investee

company for the year, duly adjusted, is

booked to the Income Statement in the

year to which the result refers.

Also, as 2012 is the year of first

application of said principle, the higher

values of the investments consequential

to the profits of previous years,

amounting to about 112 million euros,

were carried in the specific

Shareholders’ equity reserve.

The following table shows details of the

item by company.

Net exceptional expense

This item amounts to 48.8 million euros

(4.8 million euros in 2011) and refers

mainly to costs sustained for actions to

incentivise early staff resignation (62.2

million euros) partially offset by the gain

from the reimbursement of IRES

(corporate income tax) for the full

deductibility of IRAP (regional tax on

production) relating to personnel costs

and similar (12.8 million euros).

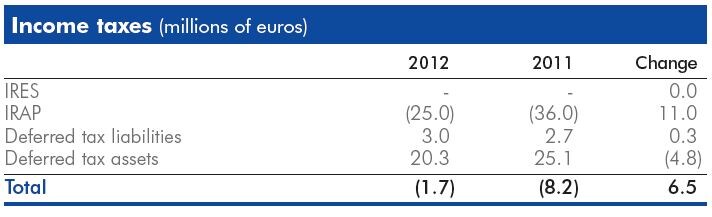

Income taxes

The item amounts to 1.7 million euros

(8.2 million euros in 2011), determined

by the balance between current and

deferred taxes, as detailed in the table.

As regards the IRES tax, no amount was

booked as the year’s result for tax

purposes was negative.

IRAP, amounting to 25.0 million euros,

shows a decrease of 11.0 million euros

compared with the previous year,

determined by a lower taxable base.

Deferred tax liabilities determine a positive

effect of 3.0 million euros (2.7 in 2011),

as a consequence of the reversal of the

temporary differences of income deriving

from the higher amortisation applied in

previous years for tax purposes only.

Deferred tax assets (20.3 million euros)

originated from the booking of IRES

credit deriving mainly from:

• the negative taxable amount, which

was offset by the positive taxable

amounts of the subsidiaries, included

within the scope of consolidation for

the 2012 tax year, with a positive tax

effect of 13.3 million euros;

• newly booked temporary differences

for programme assets, which we are

sure will be recovered in that they are

transformable into tax credits, as

provided for by paragraphs 55, 56

and 56 bis of Law Decree 225/2010,

as amended by Law Decree

201/2011, with a positive tax effect

of 8.1 million euros.

Balance sheet

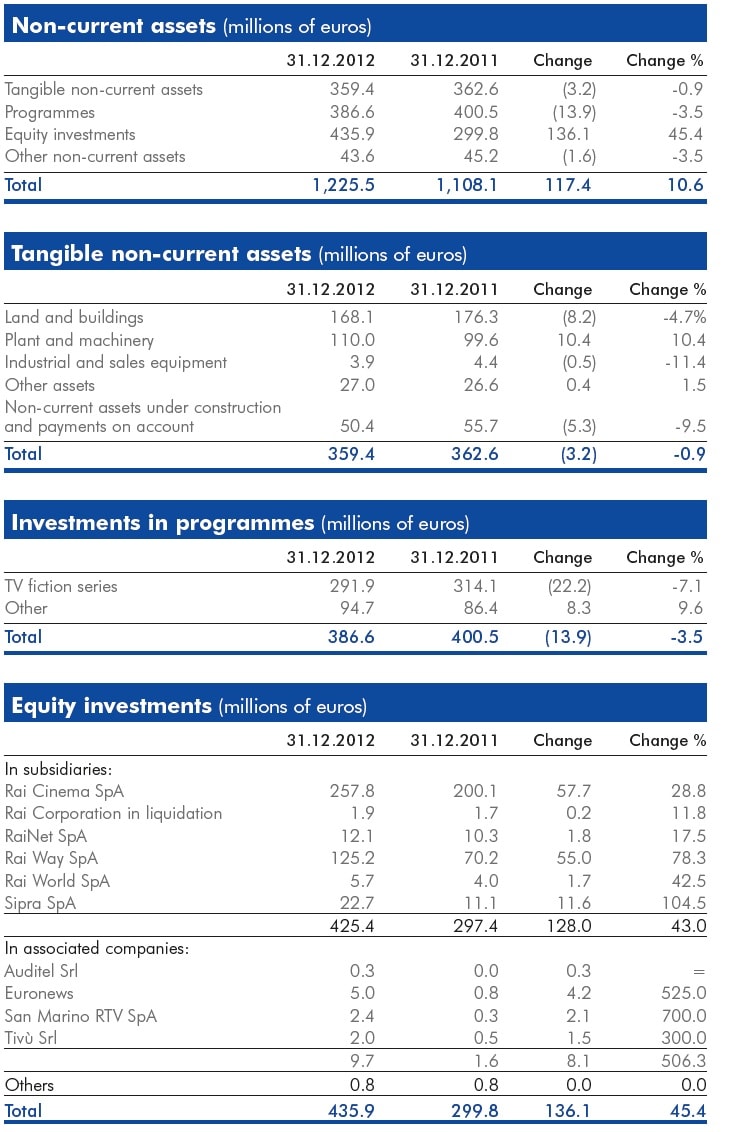

Non-current assets

Tangible non-current assets, which

have remained largely stable, are

detailed in the table below.

Investments in programmesare

mainly represented by TV fiction series

(291.9 million euros), which accounted

for the greater part of total investments

during the year (233.1 million euros).

The details are given in the table below.

Equity investments increased (+136.1

million euros) as a result of application

of the equity method to investments in

subsidiaries and associated companies,

as mentioned earlier. The details are

given in the table below.

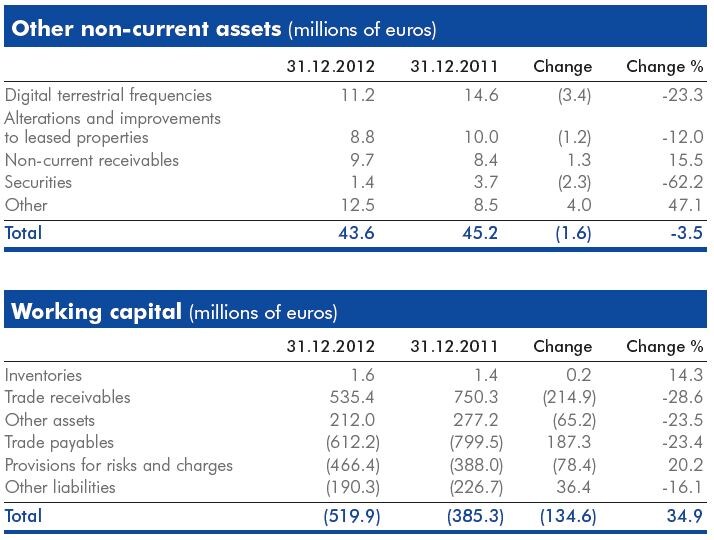

Other non-current assets, which also

remained largely stable, are detailed in

the table below.

Working capital

The change from 2011 (-134.6 million

euros) is due mainly to normal

developments in the business.

Major changes relate to:

• Trade receivables: down 214.9

million euros, due to lower amounts

of receivables from Group companies

(-124.2 million euros), mainly from

Sipra as a result of the contraction of

advertising and from minority

customers, (-90.7 million euros), the

latter determined largely by lower

receivables for special services

rendered to the Government under

contract.

• Other assets: down 65.2 million

euros largely due to the recoupment

of the advance payments made to

purchase the broadcasting rights for

sports events held during the year

(particularly the European Football

Championships and the Olympic

Games).

• Trade payables:down 187.3 million

euros, due partially to lower debts

towards subsidiaries and partially to

certain previous year’s accounts

payable to suppliers for the purchase

of sports broadcasting rights and the

DEAR property complex.

It should be noted that Trade

receivables consist mainly of accounts

receivable from subsidiaries, mainly

Sipra, and from public entities and

institutions.

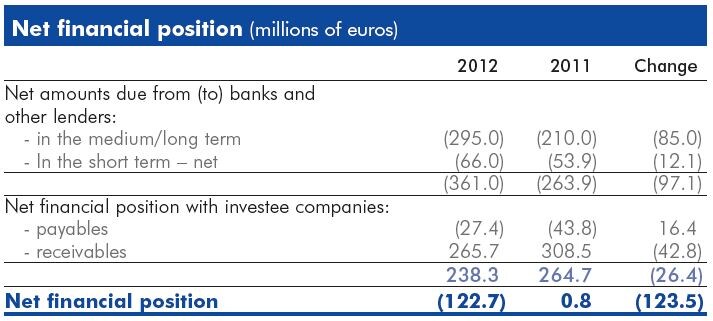

Net financial position

The year-end net financial position is

negative by 122.7 million euros,

deteriorating compared to 2011

(positive by 0.8 million euros), and is

made up as indicated in the table

below.

There was an increase in the amount

payable to banks (about 97 million

euros) and a reduction in the balance of

receivables from intercompany accounts

(about 26 million euros).

The growth of debt was caused by a

flow of activity during the year which,

due to the negative economic result, was insufficient to cover the

requirements determined by the year’s

investments. The latter include the

payment of the second instalment for

purchase of the DEAR property complex

(34 million euros).

In relation to cash flows for the year:

• the negative flows are due to the

considerable reduction in advertising

revenues, the absence of dividends

from the subsidiaries and the

application of previous charges

relating to the development of the

digital terrestrial network by Rai Way;

•the positive flows relate to the recovery

of amounts receivable for special

services rendered to the Government

under contract and the limitation of

the outlays to third parties outside the

Group for current expenses.

The unsecured loan of 295 million

euros taken out as part of a pool

envisages the respect of two

parametric/equity ratios, to be

calculated on the figures of the

consolidated financial statements, and

these ratios were respected.

The average net financial position is

negative by 55 million euros (positive by

18 million euros in 2011), with a

deterioration of 73 million euros which

is more limited than the final figure,

which reflects the more favourable

breakdown of the fee instalments,

consequential to the 100 million

increase in the amount paid with the

second and third instalments.

The analysis carried out on the basis of

the balance sheet and income

statement ratios highlighted that:

• the net invested capital coverage

ratio, determined in the ratio

between net invested capital and own

means, is 1.42 (1.00 in 2011);

• the current ratio, identified as the

ratio between current assets (inventories, current assets, cash and

cash equivalents and financial

receivables) and current liabilities

(current liabilities and financial debts),

is 1.13 (1.19 in 2011);

• the self-coverage ratio of noncurrent

assets, calculated as the

ratio of shareholders’ equity to noncurrent

assets, is 0.24 (0.39 in 2011).

The financial risks to which the

Company is exposed are monitored

using appropriate computerised and

statistical instruments. A policy regulates

financial management in accordance

with best international practices, the aim

being to preserve the corporate value by

taking an adverse attitude towards risk,

pursued via active monitoring of the

exposure and the implementation of

suitable hedging strategies, also acting

on behalf of the Group companies.

In particular:

• The exchange risk is significant in

relation to the exposure in US dollars

generated by the acquisition of sports

events rights. These commitments

generated payments for about 65

million dollars during 2012.

Operation takes place from the date

of subscription to the commercial

commitment, often lasting several

years, and aims to defend the

counter value in euros of

commitments estimated at the time of

order or in the budget. Hedging

strategies are implemented using

financial derivative instruments – such

as forward purchases, swaps and

options– without ever taking on an

attitude of financial speculation. The

Company policy envisages operating

limits to be observed by the hedging

activity.

• The interest rate risk is also

regulated by the Company policy,

particularly for medium/long-term

exposure with specific operating limits. In relation to the medium-term

loan described above, Interest Rate

Swap agreements were entered into

during 2011 for 205 million euros,

with the aim of transforming the cost

of the loan, issued at floating rate

and therefore subject to market

volatility, to fixed rate.

• The credit risk on cash deployment

is limited in that the Company policy

envisages the use, for limited periods

of cash surpluses, of low-risk financial

instruments with parties with high

ratings. Only tied deposits or sight

deposits with remunerations close to

the Euribor rate were used during

2012.

• As regards the liquidity risk, the

Company has, in the medium term, a

loan, taken out as part of a pool, for

295 million euros (expiring in 2015),

with six-monthly amortisation as of

2013. With the banking system,

short-term and reversible credit lines

were opened for a maximum amount

of about 450 million euros. Stand-by

loans are also in place for a total of

90 million euros, maturing in

February 2013. The existing loans

allow coverage of overdrafts during

the year, on condition that payment

of the fees by the Ministry of the

Economy and Finance takes place in

observance of the contractual

quarter-end deadlines. A specific

long-term loan of 100 million euros

was taken out with the European

Investment Bank to provide further

coverage of the requirements of the

progress of the DTT project during

the year. This loan will be disbursed

in two instalments during 2013.

|

|