2012 was a particularly significant year

for the evolution of the television

broadcasting market:

•

the switchover to the digital

broadcasting platform throughout

the whole of Italy was completed on

4 July. Italy now has a full digital

television broadcasting market, with

over sixty free national channels plus

local networks and pay-to-view

bouquets broadcast on the digital

terrestrial platform, which, according

to Auditel figures, reached 97% of

the population at the end of the

year;

•

the segment of live and on demand

video services and applications

available through Internet and also

available for the latest connectable

devices (smartphones, tablets, smart

tvs/decoders, etc.), which are

becoming increasingly popular, has

really taken off. Among the most

important effects, with a considerable

impact particularly on the future, the

extensive innovation of the offering

and business models, as well as the

entry of new players, often of a

global nature and from a noneditorial

background, into the sector;

•

the further consolidation of the socalled

‘social tv’ phenomenon, i.e.:

the integration between live television

and social media, also thanks to the

editorial innovation proposed by

broadcasters. While, on one hand, a

certain segment of live television is

enjoying a new season of vitality, on

the other we are witnessing the

unstoppable growth of the role and

value of the social platforms as

holders of an inestimable wealth of

knowledge of users.

The tv multi-channel format, accessibility

on several screens and platforms and

real-time interaction through the social

media have attributed even greater

value to television, which, despite the

crowded and extremely competitive

digital media context, confirms its

central role in the information and

entertainment system.

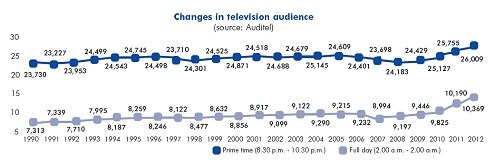

The historical record of television

consumption rose again in 2012.

According to the Auditel figures, viewing

on televisions in first homes alone rose

2% for the full day and 1% for prime

time, reaching unprecedented levels of

10.4 and 26.0 million viewers

respectively.

The inevitable redistribution of market

shares among the traditional seven

general-interest channels and new

channels continued, drawn by the

national digital terrestrial free-view

channels.

The general-interest channels (Rai 1, Rai

2, Rai 3, Canale 5, Italia 1, Rete 4 and

La7) totalled a 65.4% share, down

more than 5 points on 2011.

Compared to 2008, the year in which

the switchover to the digital platform

began, with the pilot experience in

Sardinia, these channels have fallen

almost 20 points.

In economic terms however, the year

was not particularly positive.

The worsening of the on-going

economic crisis has had a considerable

impact on the television system:

•investments in advertising fell by

14.3% (source: Nielsen Media

Research), with a performance that is

slightly worse than the total

advertising market, and the

redistribution of investments in favour

of the new free-view and pay-to-view

channels, alternative to the generalinterest

channels, was accentuated;

•

the pay-tv sector experienced a

reduction in the number of

customers, which the operators tried

to offset by raising the average level

of spending. Specifically, the leading

operator Sky ended the year with over

4.5 million households (about 18%

of the population), with a drop of

about 300,000.

Lastly, the satellite television platform

grew again.

Tivù Sat (Joint venture between Rai,

Mediaset and Telecom Italia Media),

which reached 1.7 million active cards

and 1.5 million households at the end

of 2012, as well as the substantial

elimination of Iptv, partly due to the

closure of the Fastweb service.